官方 SEC 顯示 Situational Awareness LP 已提交 Q1 2026 13F,報告期是 2026-03-31,提交/生效在 5/18。13Radar 解析顯示:披露組合約 $13.677B、42 項資產、前十大集中度 93.94%、季度換手率 32.2%。

股票/ETF 前十大重點:

BE:648.54 萬股,市值約 $8.79B,仍是最大股票倉,但減持 35.6%。

SNDK:114.01 萬股,約 $7.24B,加碼 8.2%。

CRWV:717.79 萬股,約 $5.56B,加碼 17.7%。

IREN:1169.88 萬股,約 $4.01B,加碼 34.5%。

CORZ:2600.85 萬股,約 $3.89B,減持 9.6%。

APLD:1347.84 萬股,約 $3.20B,加碼 18.9%。

RIOT/CLSK/TE 也進入前列,代表他仍把 miners / power site 當 AI data center optionality 看。

------------------------------------------------------

Leopold 這份 13F 其實不是單純「重倉股票」,而是 選擇權佔 71.8%,股票只佔 28.2%。所以他的真正打法比較像:

多 AI 基建瓶頸股 + 用大型半導體/ETF 選擇權做方向或避險

股票倉裡最清楚的三條主線是:

電力 / AI data center 能源:BE

記憶體 / 儲存瓶頸:SNDK

Neocloud / AI compute hosting:CRWV, IREN, CORZ, APLD

不過這數據是3/31的,那時候大恐慌,現在不知道調成怎樣了!

顯示更多

1. Spacex周三提交招股書, 最快 6/12 ipo 募資規模可能達 700-750 億美元,有望成為史上最大 IPO。

2.貝萊德(BlackRock)據報正考慮在 SpaceX 即將進行的 IPO 中投資 50 億至 100 億美元(約 5B-10B USD)。

3.SpaceX 初始流通股(float / 公開發行比例)預計非常低,大約只有 4%~5% 左右(部分估計 3.3%~4.3%)。

股票1拆5 高概率通過! 高概率納入納指100

另外Polymarlet上預期第一天高概率破2t

最大市值,最低流通率,然後高度控盤 ==>一龍馬的局

顯示更多

個人認為今年5-6月有機會是老馬炒作太空概念股的時間點。畢竟要配合6月的space x巨型ipo了。

3-5% 極低比例籌碼的ipo , 1.75-2t 估值的人類終極夢想。

人類去宇宙上火星,搭配宇宙資料中心概念。最美麗的夢。

搭配飛機上都能上網的星鏈。確確實實的科幻小說成真劇情。沒有比這性感的故事了。

————

另一方面,最高的ipo估值套最多的人 (nvda 是以6億估值上市的,散戶才有所謂的百倍、千倍的機會),1.7-2t 估值的ipo 散戶能有什麼機會?

而最低的比例ipo 控最完美的初期盤 。

看看六月space x ipo 走勢能否驗證猜想了。

顯示更多

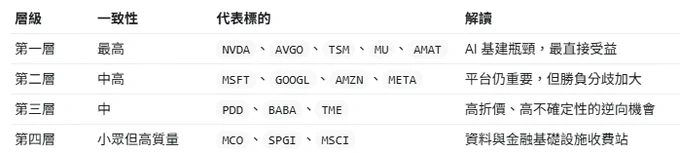

《從最新 13F 看頂尖投資人的共同下注:AI 不是答案,稀缺性才是》

Berkshire、Bridgewater、Tiger Global、Druckenmiller、李祿、段永平、Ackman 的動作看似分歧,但用第一性原理拆開,會發現他們其實都在圍繞同一件事配置:未來現金流最確定、競爭位置最稀缺、且能把 AI 時代需求轉化為高回報資本的公司。

13F 不能當即時訊號,但能看資本方向

13F 是延遲 45 天的持倉快照,不代表今天還持有,也看不到完整空單、現金和海外持倉。所以它不是抄作業工具,而是觀察頂尖資金思考框架的材料。

」

第一性原理

股票長期價值只來自三件事:

1. 未來自由現金流

2. 能否長期防守這些現金流

3. 買入價格是否合理

AI 只是技術變數,不是投資答案。投資答案要落到:誰擁有算力瓶頸?誰擁有分發入口?誰擁有資料和定價權?誰能把資本支出轉成高 ROIC?

第一個共識,AI 基建鏈

這一季最明顯的共同方向,是 AI 基建。

Bridgewater 加碼 TSM、AVGO、MU、NVDA;

Tiger Global 加碼 TSM、NVDA、AMAT、AVGO;Druckenmiller 也新增/加碼 AVGO、STM,並保留 TSM。

段永平最新可見持倉中,也大幅提高 NVDA、TSM、MSFT 的權重。

這裡的邏輯很簡單:如果 AI 需求繼續增長,最先被驗證的不是哪個應用最終勝出,而是整個產業都需要更多晶片、代工、記憶體、網路與電力效率。

第二個共識,平台股仍重要,但分歧加大**

大型平台股不是被拋棄,而是進入分化。

Berkshire 大幅加碼 Alphabet,李祿也把 Alphabet 放在極高權重;但 Ackman 幾乎賣出 Alphabet,轉去買 Microsoft;Druckenmiller 則退出 GOOGL、減碼 Amazon。

這代表市場不是否定平台股,而是在重新評估:誰能把 AI 投入變成真實現金流?

Google 有搜尋、YouTube、雲端和 Gemini 生態;Microsoft 有 Azure、Office、OpenAI 關係和企業分發;Amazon 有 AWS 和電商現金流;Meta 有廣告分發和 AI 推薦效率。

大家都知道平台重要,但對哪個平台的邊際回報最高,答案並不一致。

第三個共識,低估的中國平台仍被少數高手買入**

李祿重倉 PDD,段永平也加碼 PDD,同時仍持有 Alibaba。這說明中國平台沒有被全部放棄,而是被高度選擇性地買入。

中國平台公司的問題不是商業模式失效,而是折價過重:政策風險、地緣風險、消費信心和資本市場信任度,都壓低了估值。

但如果一家公司仍有高 ROIC、強現金流、低估值和長期競爭優勢,那它就會進入深度價值投資人的視野。

三位關鍵人物

段永平的組合仍以 Apple 和 Berkshire 為核心,但增量資金明顯偏向 AI 基建和中國平台。他買的不是短期熱點,而是強產品、強生態和長需求。

Druckenmiller 則代表另一種訊號。他不是長期抱死,而是宏觀輪動。他加碼 Natera、YPF、AVGO、STM,退出 GOOGL,減碼 Amazon。這說明 AI 基建仍有吸引力,但大型平台股要更挑位置與估值。

李祿最集中,也最像 Munger 系投資人。他重倉 Alphabet、PDD、Berkshire,同時新買 Moody’s、S&P Global、MSCI 這類資料與金融基礎設施公司。這些公司本質上是資訊收費站。

真正的結論

這些頂尖投資人的共同下注,不是「AI 會漲」,而是:

縮減投資數量,提⾼集中度。

重壓關鍵節點:算力瓶頸、平台入口為主!

顯示更多

台灣嘻哈教父黃立成(@machibigbrother)在 X 宣布:「Honored to join Shark Tank.」,正式成為《Shark Tank Taiwan》五位投資人之一。

其他四位投資人為:台灣大哥大總經理林之晨、和鼎創投劉奕成、Relove 共同創辦人古婉蓁、日本 Headline Asia 創始合夥人田中章雄。

由緯來電視網與 Sony Pictures 合作推出的創業實境秀,麻吉大哥憑藉音樂、直播與 Web3 跨界經驗加入,預計下半年開播。

顯示更多

bill ackman喊盤微軟

認為此時如同2022年chatgpt剛出時google被低估一樣。

微軟處於價投好位置。

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

顯示更多

這訪談真不錯

Semi Maxi(半導體至上)

AI 才剛開始,缺貨會持續很久很久

最強配置:光模組 + Intel + 台積電 + 中國存儲

回調就是買點,長期極度樂觀

spv仲介費用,還真不輸給銀行的理專

You invested $100K via a 3-layer Anthropic SPV at $380B valuation.

Third layer takes 15% management/set up fees and no carry

Second layer takes 10/20

First layer takes 10/20

So your real investment is 100*0.85*0.9*0.9=$68.85K. Given nobody scammed anyone in the matryoshka

An exit at $1.4T IPO gets you a MOIC of ~2.8x after dilution. That’s $192K on the first layer.

The first layer takes 20% carry, you have $167K left

The second layer takes 20% carry ($36.4k), you have $130.6k left

So you have made a $30K return on a $100K investment in a year.

So layered SPV investment got you a 68% Anthropic exposure. Buying Google stock gets you 14% and Amazon - 18%. AND a multiple on all the money Anthropic spends on compute (most of their money). AND exposure to a money-printing business with a strong AI component that rivals Anthropic. AND no scam risk. While the 32% lost in SPV fees just fund someone’s coke habit in Miami.

Same $100K put in AMZN and GOOG over the same time period would also get you the 30% return. You’re welcome.

顯示更多

大家最近都在問 5 月有什麼好項目?首推 Everything!這個月他們火力全開,一口氣上線三個重磅活動。無論你是想零擼簽到,還是想靠預測技術致富,這波絕對不能錯過。

💡 核心利益點:

每天進入平台簽到即可領取 20 $E,目前的市場參考價值約 4.6u。每天動動手指,這豬腳飯不就有了嗎?

🔥 活動一:Daily Streak Frenzy (4/27 – 5/27)

這是最簡單的「零擼」玩法,主打一個堅持。

玩法: 每天進入平台進行簽到。

收益: 每日固定領取 20 $E。

小秘訣: 這次活動官方鼓勵「有量」,建議大家可以自己刷一點 Everything 交易量(簡單開關倉位,幾乎無磨損),這對提升賬號權重非常有幫助!

🔮 活動二:Prediction Madness (5/15 – 6/15)

喜歡看盤、猜漲跌的朋友,這是你們的戰場!

玩法: 針對熱門幣種進行價格預測。

亮點: 展現你的交易實力,預測準確率越高,獎勵越豐厚。

🚀 預告:Everything Earn (5/21 啟動)

月底還有大招!Everything Earn 將正式上線,預計會提供更高階的收益玩法。現在趕快簽到積攢 $E,為 Earn 的上線做好準備。

📌 參與方式:

點擊我的專屬連結:

每日簽到,領取 20 $E。

進行簡單交易,刷出賬號活躍度。

@trdEverything @trdEverythingCN #Everything# #Crypto# #Airdrop#

顯示更多

The Futures Trading Leaderboard ends tomorrow.

$1,000 in USDT rewards are on the line each week.

Who will take the top prize? 🏆

這次川川訪中可謂巨商雲集

zero hedge 說了 一艘飛機上有20兆美金的ceo

老馬回了只有我跟Jensen (老黃)

可以解釋成空軍一號只有他們兩個?

還是老馬是說只有他們兩個人夠有錢?

另外老黃是最後一刻才受邀。

預計也是美中 芯片封禁有所進展了

顯示更多

@zerohedge Just Jensen and I are on AF1

這次 Four Meme AI Sprint 我其實有點意外。

@fourdotmemezh

幣圈現在很涼 ,大家都說「喊 AI 敘事、實際沒產品」的黑客松,但最後從 196 個 BUILDs 裡面殺進決賽的幾個項目,看得出來整個方向其實蠻明確的——不是空談 Agent,而是開始有人真的在做「能用、能互動、能長出社群」的 AI Meme Product。

現在市場其實不缺 AI,缺的是「有流量入口的 AI」。 所以這次 Four meme 提供的不只是 5 萬美元獎金,真正重要的是它背後能給項目的: 生態曝光 社群流量 BNB Chain 資源 meme 傳播能力 early users 這個其實比單純獎金更重要。

我自己看這次 Top 5,有幾個方向蠻值得聊。 像是 @4lpha_agent,算是比較偏 AI Agent execution 的路線。 現在市場很多 Agent 都停留在「會聊天」,但真正有價值的是能不能幫使用者做事情。 如果未來能再往鏈上互動、自動化交易、資訊整合去延伸,我覺得這類型項目其實有機會變成下一輪 AI + Crypto 的基礎入口。 另外我覺得 ClipX 也蠻有意思。 因為現在注意力市場很碎片化,AI 如果只是「生成內容」其實已經不夠了。 真正重要的是: 能不能降低創作者做內容的成本,同時提升傳播效率。

但我覺得整場黑客松最值得注意的,還是 本身的方向。 現在很多平台都在講 AI。 但 比較特別的是,它開始嘗試把: 「AI Builder + Meme Culture + 社群傳播」 這三件事情綁在一起。 這其實是對的。 而 meme,本來就是 crypto 世界最強的流量引擎之一。 所以這次 AI Sprint 某種程度上,比較像是在提前測試: AI Meme 生態到底能不能真的長出東西。 至少目前看起來,方向比很多人想像中更認真。 也恭喜所有進入決賽的團隊。 從 196 個 BUILDs 走到最後,其實已經不只是 idea 了,而是真的有人開始 build。 市場現在很浮躁。 但真正能活下來的,通常還是那些: 願意持續做產品的人。

顯示更多

🏆 The Top 5 finalists of the AI Sprint are officially here.

(In alphabetical order, not final ranking)

• 4lpha AI @4lpha_agent

• Build4 @build4ai

• Clawdyland @clawdyland

• ClipX @ClipX0_

• elizaOK @elizaok_bsc

From 196 BUIDLs to the final 5 — thank you to every builder who participated in this sprint 🤍

As a reminder, final results are determined based on combined judge scoring + community voting, with all non-compliant votes removed during the review process to ensure fairness and accuracy.

Final rankings and 5 community engagement awards will be revealed on Demo Day.

🕛 13 May, 12PM (UTC+8)

Stay tuned 👀

顯示更多

今年下半年是美股大ipo期

@bitget

上次的prime ipo space x

噴了20%

這次推出另一個巨型ipo prime

openai

估計還是能賺錢的 大家可以參考看看

顯示更多

沒人要防守了

防禦型股票

消費必需品+醫療保健+公用事業合併目前僅佔 S&P 500 市值約 15%,為1970 年代以來最低。

目前處於全民投三分,跑轟 場均150+ 進攻狀態。

顯示更多

Defensive stocks have never been this disliked:

The healthcare sector now accounts for just 8.3% of the S&P 500’s market cap, the lowest percentage since 1994.

Their weight has fallen by -50% since the 2022 bear market.

By comparison, healthcare represented ~9.0% of the index’s value at the 2000 Dot-Com Bubble peak.

Furthermore, consumer staples, healthcare, and utilities collectively now account for just ~15% of the S&P 500’s market cap, the lowest since at least the 1970s.

Their weighting has dropped -12 percentage points since 2022, marking an even bigger drop than during the Dot-Com run.

Tech stocks have never been bigger.

顯示更多

Larry Fink 就是說

我們缺電力、缺芯片、缺算力

什麼都缺

所以他想開始搞算力期貨了…

LARRY FINK JUST PREDICTED A NEW ASSET CLASS

The BlackRock $BLK CEO laid out where he sees the bottleneck of the AI buildout at the Milken Institute.

His framing of the problem:

"The United States is short power, short compute, short chips. There are going to be shortages in all three. We just don't have enough compute power right now."

His prediction for what comes next:

"I actually believe a new asset class will be buying futures of compute."

Compute futures do not exist as a standardized tradable contract today. Fink is calling out the emergence of one.

顯示更多

個人認為今年5-6月有機會是老馬炒作太空概念股的時間點。畢竟要配合6月的space x巨型ipo了。

3-5% 極低比例籌碼的ipo , 1.75-2t 估值的人類終極夢想。

人類去宇宙上火星,搭配宇宙資料中心概念。最美麗的夢。

搭配飛機上都能上網的星鏈。確確實實的科幻小說成真劇情。沒有比這性感的故事了。

————

另一方面,最高的ipo估值套最多的人 (nvda 是以6億估值上市的,散戶才有所謂的百倍、千倍的機會),1.7-2t 估值的ipo 散戶能有什麼機會?

而最低的比例ipo 控最完美的初期盤 。

看看六月space x ipo 走勢能否驗證猜想了。

顯示更多

SpaceX IPO:Musk 與內部人士鞏固投票控制權

雙重股權結構(Dual-Class Structure)

SpaceX 計畫在 IPO 後透過超級投票股(super-voting shares)鞏固 Musk 的控制權。

根據 Reuters 取得的招股書摘要,採用雙重股權結構:

Class B 股每股擁有 10 票,集中於 Musk 及少數內部人士手中;

而賣給公眾投資人的 Class A 股每股只有 1 票。

結果是 Musk 持有約 42% 的股權,但透過超級投票股掌控約 79% 的投票權。

IPO 規模與目標

SpaceX 目標上市估值約 1.75 兆美元,募資 750 億美元,若成功將成為史上最大 IPO。

Musk 的角色與薪酬

IPO 完成後,Musk 將繼續擔任 CEO、CTO,並出任 9 人董事會主席。雖然他去年薪資僅 54,080 美元,但上市後將透過股權獲益數十億美元。

對公眾股東的限制

招股書中也列出了限制股東影響力的條款,包括強制仲裁、限制法律訴訟場所等,公眾股東實際上無法影響公司策略方向。

SpaceX + xAI 合併的新故事

值得注意的是,SpaceX 在 2026 年 2 月以全股票交易收購了 Musk 的 AI 新創 xAI(X 的母公司),合併實體估值達 1.25 兆美元。這使 SpaceX 的 IPO 敘事從純粹的火箭/衛星公司,擴展為同時包含 AI 基礎設施的投資標的。

------------------------------

比較特別的,大概就是TGE 目前S1 還沒公佈但大概率是3-5% , 歷史最大的IPO 搭配極低的初始釋放!

Nasdaq 已移除 10% 流通股的門檻要求,並新增「快速納入」機制——若公司市值排進指數前 40 大,可在 IPO 後 15 個交易日內被納入。所有變更從 5 月 1 日起生效。 SpaceX 估值 1.75 兆美元,輕鬆進前 40,這條規則幾乎就是為它量身定做的。

目前預測市場評估該公司在 2026 年 6 月 30 日前完成 IPO 的機率高達 74.5%,市場共識估值落在 1.5 兆至 2.5 兆美元之間

承銷商為美國銀行、高盛、摩根大通與摩根士丹利。

關於估值的三點觀察

第一,2 兆美元即便放在 AI 時代也是極端的。 以目標估值計算,SpaceX 185 億美元的年收入對應市銷率(P/S)為 108 倍。

相比之下,Nvidia 在 2024 年 AI 熱潮巔峰時的市銷率約為 40 倍。

SpaceX 的 IPO 市銷率將是 Nvidia 巔峰值的近 3 倍。Meta IPO 時的市銷率約 30 倍,而且Spacex仍持續虧損。

第二:最美的故事, 發射業務(獵鷹 9 號、獵鷹重型、星艦):全球主導地位。

Starlink:約 110 億美元年收入,成長快速。

xAI(已併入 SpaceX):原本獨立運營的 AI 業務。

國防合約:NASA、美國國防部、盟國政府。

軌道數據中心:尚在畫餅階段,但獲得機構認可的聲音越來越多。發射能力+衛星基礎建設+AI+國防的整合故事,目前沒有其他公司能複製。

以極端估值上市的 IPO,爽到的是:早期投資人、員工與 IPO 前的股東。這些都是退出事件。IPO讓所有散戶接盤了!

但極低的初始釋放, 極高可能拉高前幾天的fomo情緒!!但類似的大型IPO 過去情形:

四個最具代表性的大型IPO規律:

首週走勢:兩種極端

Alibaba 首日開盤 $92.70,漲幅超過 35%,首週一度觸及 $120(+76%)

Facebook 則相反——首週收在 $31.91,比 IPO 價低了 16%

Google 和 Saudi Aramco 首週溫和上漲 18%~19%

一年後:幾乎全跌 , 甚至腰斬!!

而且Space X 前期獲利盤太多,有強大的解鎖壓力!!估計腰斬也是差不多的!!

顯示更多

妥妥的紙手病

知道死拿到ipo前fomo大概率能賺錢

但一樣紙手!!

@bitget

SpaceX IPO:Musk 與內部人士鞏固投票控制權

雙重股權結構(Dual-Class Structure)

SpaceX 計畫在 IPO 後透過超級投票股(super-voting shares)鞏固 Musk 的控制權。

根據 Reuters 取得的招股書摘要,採用雙重股權結構:

Class B 股每股擁有 10 票,集中於 Musk 及少數內部人士手中;

而賣給公眾投資人的 Class A 股每股只有 1 票。

結果是 Musk 持有約 42% 的股權,但透過超級投票股掌控約 79% 的投票權。

IPO 規模與目標

SpaceX 目標上市估值約 1.75 兆美元,募資 750 億美元,若成功將成為史上最大 IPO。

Musk 的角色與薪酬

IPO 完成後,Musk 將繼續擔任 CEO、CTO,並出任 9 人董事會主席。雖然他去年薪資僅 54,080 美元,但上市後將透過股權獲益數十億美元。

對公眾股東的限制

招股書中也列出了限制股東影響力的條款,包括強制仲裁、限制法律訴訟場所等,公眾股東實際上無法影響公司策略方向。

SpaceX + xAI 合併的新故事

值得注意的是,SpaceX 在 2026 年 2 月以全股票交易收購了 Musk 的 AI 新創 xAI(X 的母公司),合併實體估值達 1.25 兆美元。這使 SpaceX 的 IPO 敘事從純粹的火箭/衛星公司,擴展為同時包含 AI 基礎設施的投資標的。

------------------------------

比較特別的,大概就是TGE 目前S1 還沒公佈但大概率是3-5% , 歷史最大的IPO 搭配極低的初始釋放!

Nasdaq 已移除 10% 流通股的門檻要求,並新增「快速納入」機制——若公司市值排進指數前 40 大,可在 IPO 後 15 個交易日內被納入。所有變更從 5 月 1 日起生效。 SpaceX 估值 1.75 兆美元,輕鬆進前 40,這條規則幾乎就是為它量身定做的。

目前預測市場評估該公司在 2026 年 6 月 30 日前完成 IPO 的機率高達 74.5%,市場共識估值落在 1.5 兆至 2.5 兆美元之間

承銷商為美國銀行、高盛、摩根大通與摩根士丹利。

關於估值的三點觀察

第一,2 兆美元即便放在 AI 時代也是極端的。 以目標估值計算,SpaceX 185 億美元的年收入對應市銷率(P/S)為 108 倍。

相比之下,Nvidia 在 2024 年 AI 熱潮巔峰時的市銷率約為 40 倍。

SpaceX 的 IPO 市銷率將是 Nvidia 巔峰值的近 3 倍。Meta IPO 時的市銷率約 30 倍,而且Spacex仍持續虧損。

第二:最美的故事, 發射業務(獵鷹 9 號、獵鷹重型、星艦):全球主導地位。

Starlink:約 110 億美元年收入,成長快速。

xAI(已併入 SpaceX):原本獨立運營的 AI 業務。

國防合約:NASA、美國國防部、盟國政府。

軌道數據中心:尚在畫餅階段,但獲得機構認可的聲音越來越多。發射能力+衛星基礎建設+AI+國防的整合故事,目前沒有其他公司能複製。

以極端估值上市的 IPO,爽到的是:早期投資人、員工與 IPO 前的股東。這些都是退出事件。IPO讓所有散戶接盤了!

但極低的初始釋放, 極高可能拉高前幾天的fomo情緒!!但類似的大型IPO 過去情形:

四個最具代表性的大型IPO規律:

首週走勢:兩種極端

Alibaba 首日開盤 $92.70,漲幅超過 35%,首週一度觸及 $120(+76%)

Facebook 則相反——首週收在 $31.91,比 IPO 價低了 16%

Google 和 Saudi Aramco 首週溫和上漲 18%~19%

一年後:幾乎全跌 , 甚至腰斬!!

而且Space X 前期獲利盤太多,有強大的解鎖壓力!!估計腰斬也是差不多的!!

顯示更多

曾經的傳奇kyle 哥,退出multi coin了。

當初10刀以下喊買進sol的傳奇….

話說當初我zama 有一定的部分也是被kyle 影響到。

唉,也是希望 zama 拉一拉了。

還有幣圈能有下個10刀以下sol

顯示更多