LIWEI_TW Capital

@LIWEI_TWCapital

Focusing on photonic stocks until 2027: $AAOI, $SIVE, Shunsin (TWE:6451)

Joined January 2024

219 Following 2.8K Followers

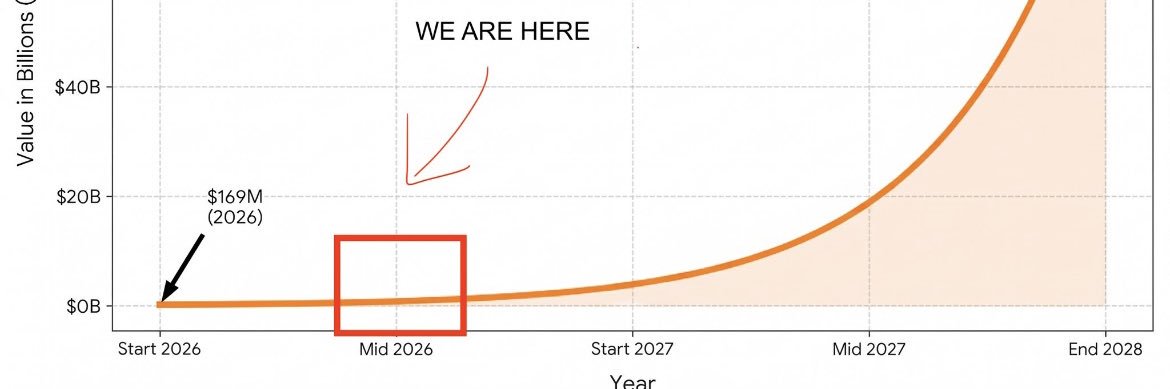

MssCorp (TWE: 6830) Serenity High Conviction Bet(analysis fully grounded in TSMC’s latest public expansion plans and 2026 industry data):

– this is the functional monopoly in CPO/SiPh inspection (90%+ share targeted, pricing power is real). Long list of customers ($TSM, $NVDA, $AAPL, $AMAT , $LRCX, $ASML , $INTC ) all need to go through them for yields. NVIDIA dedicated AI Chip Zone in US facility = strategic lock-in.

-GS CPO TAM still the anchor: $91B by 2028.

-TSMC CoWoS doubling to 130k-140k wafers per month by end-2026 via AP7 Chiayi (world’s largest advanced packaging hub, CoPoS pilot 2026/volume ramp 2027-28) + AP8 Tainan (P1/P2) + AP5/AP6 upgrades. We are still in the frontrunning window.

Pure TSMC fab expansion model only — no NVIDIA exclusive assumed. Factory-by-factory HG demand: HG is specialized QA/FA tool (not standard per-line gear). Base Assumption~60 units per major packaging “module group” (20 front / 20 mid / 20 back).

Using latest TSMC 2026 data:

AP6 (Longtan/Taichung): Operating + upgrade → ~30 units / MssCorp 25-30 units

AP7 Chiayi: World’s largest, CoPoS pilot → ~45-120 units / MssCorp 40-100 units

AP8 Tainan (P1-P2): Construction/ramp → ~120 units/ MssCorp 100-110 units

AP8 later phases + AP9: 2028+ planning → ~240-260 units / MssCorp 200-220 units

TSMC only total: ~435-530 units / MssCorp 365-460 units

Updated HG model (reflecting monopoly + pricing power): Industry total demand 130-200 units 26-30. With 90%+ monopoly → MssCorp ships 120-180 units (spares + repeat buys). ASP NT$60M (pricing power) + GM 60-75%.

HG contribution build (NT$ bn, cumulative 2026-2030): Equipment sales + Recurring services/consumables (25–45% of equipment value over 5 years) + IP licensing (20–35% of equipment rev, 80-90% margin). Total HG contribution NT$9.5bn–NT$13bn. Core MA/FA business growing 20-30% CAGR from NT$22B 2025 base on top.

Revenue path (NT$ bn):

2026: 30–38

2027: 45–62

2028: 65–88

2029-30+: 180–240/yr (normalized)

Mix shifts hard to high-margin equipment + recurring + IP as CPO goes volume

Share count 51.78M. With the structural monopoly in a critical yield choke-point + TSMC/NVIDIA tailwinds, long-term normalized forward EPS can realistically reach NT$180–240 (US$5.6–7.5).

40–60x forward P/E (standard for AI/SiPh leaders with real moats) → target NT$5,000+. Current MC ~$1.2–1.4B.

Show more