LIWEI_TW Capital

@LIWEI_TWCapital

Focusing on photonic stocks until 2027: $AAOI, $SIVE, Shunsin (TWE:6451)

219 Following 2.8K Followers

Jensen Huang is visiting Taiwan again.

Key keyword: Edge Computing, Feynman

Is The Age of edge devices/Robotics coming ??

Some Indian guy really is clueless about semiconductors… he clearly has no idea what he’s talking about. No wonder the Taiwan market bounced back right away today. It’s pretty obvious who’s being delusional here.

Show more

“Taiwan won’t matter in 18 months” is what happens when software people mistake civilization for a SaaS product.

It's one of the most clueless takes I've heard on this platform in months and that's saying something.

Yes, America has semiconductor fabs. Mostly old ones. Really old.

Taiwan has the fabs that matter:

The ones that make every single chip for NVIDIA and Apple and every damn Android and iPhone on Earth and even most of the 1500 or so chips that go in your truck or car.

Without TSMC these companies simply do not exist. Not kind of struggling. I mean "wiped off the freaking face of the Earth and unable to produce a single product" level gone.

As in "worth zero instantly."

Taiwan has:

- Multiple leading-edge giga-fabs

- The *overwhelming* majority of advanced AI chip production

- Dominant advanced packaging capacity

- Dense supplier clustering

- Decades of accumulated yield/process knowledge and the most skilled workforce on Earth to run it all

The US still barely has frontier-scale advanced packaging online. Much of it is literally still under construction and won’t ramp until years from now.

Momos hear “we’re only 1–2 nanometers away” and think semiconductors are just transistor geometry.

No freaking way. Sheer idiocy. The real moat is:

- Yields

- Packaging

- HBM integration

- Substrates

- Tooling

- Tacit manufacturing expertise

- Workforce density

- Supply chain coordination

TSMC is not “a fab.” It is one of the most sophisticated industrial ecosystems ever created by humanity.

And no, a tiny Neuralink surgery robot does not mean America can magically reproduce decades of semiconductor manufacturing concentration in 18 months.

Reality is not a podcast episode.

Taiwan remains strategically critical for years, likely a decade+.

This is like saying:

“We’re 18 months away from replacing the global oil system because we built a nice electric bike.”

Show more

$POET and $IREN literally both won the Fake it Until you make it award.

-> Grey area endless marketing of crap through influencers.

-> Diluted retail enough to hoard tons of cash

-> Cash is sets baseline Market Cap.

Now $POET probably has around $830M pure cash from dilution after $400m private placement.

While their marketcap was sitting under $500m last year.

Show more

MssCorp (TWE: 6830) Serenity High Conviction Bet(analysis fully grounded in TSMC’s latest public expansion plans and 2026 industry data):

– this is the functional monopoly in CPO/SiPh inspection (90%+ share targeted, pricing power is real). Long list of customers ($TSM, $NVDA, $AAPL, $AMAT , $LRCX, $ASML , $INTC ) all need to go through them for yields. NVIDIA dedicated AI Chip Zone in US facility = strategic lock-in.

-GS CPO TAM still the anchor: $91B by 2028.

-TSMC CoWoS doubling to 130k-140k wafers per month by end-2026 via AP7 Chiayi (world’s largest advanced packaging hub, CoPoS pilot 2026/volume ramp 2027-28) + AP8 Tainan (P1/P2) + AP5/AP6 upgrades. We are still in the frontrunning window.

Pure TSMC fab expansion model only — no NVIDIA exclusive assumed. Factory-by-factory HG demand: HG is specialized QA/FA tool (not standard per-line gear). Base Assumption~60 units per major packaging “module group” (20 front / 20 mid / 20 back).

Using latest TSMC 2026 data:

AP6 (Longtan/Taichung): Operating + upgrade → ~30 units / MssCorp 25-30 units

AP7 Chiayi: World’s largest, CoPoS pilot → ~45-120 units / MssCorp 40-100 units

AP8 Tainan (P1-P2): Construction/ramp → ~120 units/ MssCorp 100-110 units

AP8 later phases + AP9: 2028+ planning → ~240-260 units / MssCorp 200-220 units

TSMC only total: ~435-530 units / MssCorp 365-460 units

Updated HG model (reflecting monopoly + pricing power): Industry total demand 130-200 units 26-30. With 90%+ monopoly → MssCorp ships 120-180 units (spares + repeat buys). ASP NT$60M (pricing power) + GM 60-75%.

HG contribution build (NT$ bn, cumulative 2026-2030): Equipment sales + Recurring services/consumables (25–45% of equipment value over 5 years) + IP licensing (20–35% of equipment rev, 80-90% margin). Total HG contribution NT$9.5bn–NT$13bn. Core MA/FA business growing 20-30% CAGR from NT$22B 2025 base on top.

Revenue path (NT$ bn):

2026: 30–38

2027: 45–62

2028: 65–88

2029-30+: 180–240/yr (normalized)

Mix shifts hard to high-margin equipment + recurring + IP as CPO goes volume

Share count 51.78M. With the structural monopoly in a critical yield choke-point + TSMC/NVIDIA tailwinds, long-term normalized forward EPS can realistically reach NT$180–240 (US$5.6–7.5).

40–60x forward P/E (standard for AI/SiPh leaders with real moats) → target NT$5,000+. Current MC ~$1.2–1.4B.

Show more

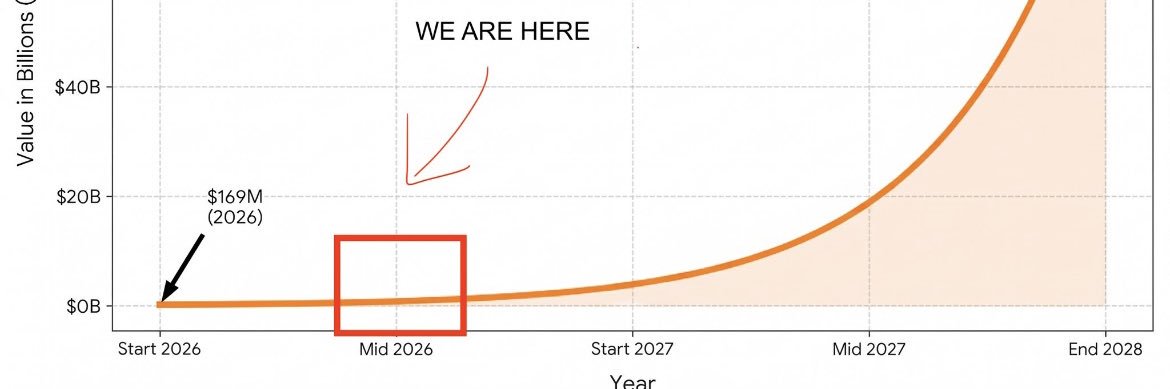

FII Vera Rubin Rumor & CPO Order Upgrade for Shunsin (TWE:6451):

• Unofficial source (FII Earnings Call’s lunch gathering ) claim FII has secured major involvement in NVIDIA’s Vera Rubin platform (August mass production, ~60% share on key components, doubled GB server shipments to ~60k units, and >10k racks).

• Taiwanese media (Economic Daily News, May 13) reports Foxconn has begun early CPO full-optical switch shipments to NVIDIA, with targets sharply upgraded to over 50,000 units combined for 2026–2027 (from original ~10k estimate).

• Shunsin (TWE:6451), Foxconn group’s key subsidiary for high-speed optical transceiver modules and CPO technology, is positioned in the “optics” segment that FII is reportedly sourcing externally while integrating most other components in-house.

• If realized, the elevated CPO volumes could drive increased intra-group demand for Shunsin’s optical interconnect solutions.

Conclusion: This combination points to another potential positive development for Shunsin (TWE:6451) within the Foxconn AI supply chain..

Show more

#市場小作文# #RUMOR#

工业富联午餐交流反馈

业绩:4月单月营收突破1000亿,上半年突破5000亿

Vera Rubin交货进展

-Vera Rubin没有延期,为了做得更好,组装有一些改样,8月量产,9月出货

-富联做了6成份额,做了两个大客户,都是独供

-Switch 和 compute tray都是富联做的,midplane 也是富联做的,就剩一个光

-Compute tray midplane 已经开始生产,用的胜宏板子,44层,这是个标准品,所有CSP代工厂都要跟富联买

-VR现在一个柜子1800公斤,单价700-800万美金

-存储柜子富联做的比较多

英伟达服务器出货量

-GB 今年出货量翻倍,达到6万台;VR今年出货量会远超1万台

英伟达服务器零部件

-富联增加垂直整合能力,富联自己可以做冷却系统,电源系统,增加获利能力,不会是富联独供,也会分出去

-英伟达服务器内部60-65%零部件可以自己做,但其中一半会从外面买,争取剩下30%多自己做,现在已经有20%多是自己做了,后面还有10个点提升空间,这些产品毛利率通常高过15%

重视自动化和电源

-富联今年CAPEX 超过500亿,光自动化设备就会有300亿(强瑞,安达,博众,汇川),强瑞和安达智能很快就会接到很多单子

-数据中心最大考验是电力,以前不能投资电力,现在开始自己投资电力

-新厂在建设800V(从400V变800V),要考虑能耗,比较省电,效率比较高,需要考虑SiC的变化

-存储一定会有问题,长鑫产能包出去了都不够,预计2-3年还会有挤压

ASIC服务器进展

-asic 机柜营收过去占比是20%,今年占比超过30%

-1Q26 asic机柜营收翻了三倍

-富联来自谷歌和AWS的收入今年都会翻倍

CPO

-今年努力做到1万台,好几个工厂在不同地区做这个;明年做几万柜。

#零級分#

Show more

We visited $POET's HQ building in Toronto. We found abandoned rooms and none of the tenants on the same floor recognized POET.

Most foreign investors really didn’t realize this….

NVDA’s 50k-unit CPO full-optical switch order is a

50,000 Unit* 100,000 USD/per Unit=5 billion USD PO….

Yet Shunsin ( the critical Foxconn CPO packaging player, has a market cap of only < $2B…

#foxconn#, #NVDA#

Show more

Taiwanese media reports that Foxconn has begun early shipments of all-optical CPO switch racks to NVIDIA, with shipment forecasts revised upward from the prior 10,000+ units in 2026 to 50,000+ units across 2026–2027.

According to industry sources, Hon Hai Group is producing the all-optical CPO switch racks at its Vietnam plant and has already begun early shipments to NVIDIA. Supply is reportedly extremely tight — even the units originally allocated for demo purposes have been diverted to NVIDIA, leaving "not a single rack to spare."

Show more

TSMC 2026 Technology Symposium (Taiwan 5/14) Summary:

Global Expansion & Operations

· Global Build-out: Constructing or modifying 18 fabs worldwide (includes 5 advanced packaging plants).

· Taiwan Core: 12 of these 18 facilities are located in Taiwan.

· Acceleration: Expansion speed has doubled to 9 new plants per year (2025–2026) vs. 4 per year (2017–2024).

International Site Progress

· Arizona (USA):

-Fab 1 output to grow 1.8x in 2026.

-Fab 2 equipment move-in 2H-2026 (N3 production 2H-2027).

-Fab 3 broke ground 1H-2025.

-Fab 4 and first advanced packaging plant (AP1) are in initial construction.

· Kumamoto (Japan):

-Fab 1 (28/22nm) yield already equals Taiwan levels; 2026 output target is 2.3x YoY.

-Fab 2 began construction in 2025 for N3 production.

· Dresden (Germany):

-ESMC facility focusing on 12nm–28nm for Automotive/Industrial.

Advanced Process Roadmap (N2 / A14 / A12)

· N2 Momentum: Fab 20 (Hsinchu) and Fab 22 (Kaohsiung) are in mass production. Taichung Fab 25 to follow in 2028.

· N2 Performance: First-year output expected to be 45% higher than N3's first year. Capacity expansion CAGR of 70% seen 2026–2028.

· Yield Maturity: N2 yield learning curve is 2 quarters ahead of N3 at the same stage, driven by AI-optimized manufacturing.

· A14 (1.4nm): Already achieved >80% yield on 256Mb SRAM; offers 10–15% speed boost or 25–30% power reduction vs. N2.

· New Nodes:

-A12 (Performance-focused with Backside Power/Super Power Rail) and A13 both targeting 2029 production.

-N2U(enhanced 2nm) slated for 2028.

· Next-Gen: CFET architecture reduces SRAM cell area by 30%vs. Nanosheet.

Advanced Packaging & Silicon Photonics

· CoWoS Scale: 5.5x reticle size now at 98% yield. Scaling to 14x reticle for 20 HBMs by 2028 and 24 HBMs by 2029.

· System on Wafer (SoW): Future "Super Exchange" chips to integrate 64 HBMs/16 CoWoS units, exceeding 40x reticle size with 100TB+ bandwidth.

· Growth: 3DIC/CoWoS capacity CAGR of >80% 2022–2027.

· COUPE: All-optical interconnects to replace copper as data centers scale to millions of GPUs and power needs surge 200x.

Specialty & Memory Shift

· The Memory Divorce: Shifting from eFlash to RRAM (ReRAM) and MRAM for advanced nodes (≤28nm) in Auto, AI Glasses, and Edge AI.

· Edge AI Specs:

-N4PRF (RF process) for 39% power reduction

-N16HV(16nm High Voltage) specifically for AI Smart Glasses/AR displays.

$TSM $NVDA $AAPL $AMD $AVGO $MRVL $INTC $AMZN $GOOGL $MSFT $META #semiconductors#

Links:

Show more

You guys should have listened…

Serenity’s High Conviction Bet: ShunSin ( – Pre-Market Supplement:

I have a few quick points to add before the market opens. Hope everyone uses today’s earnings volatility as the perfect chance to get on board!

1. Earnings Loss Interpretation:

According to TWSE (Taiwan Stock Exchange) rules, stocks that enter “disposition” must publish monthly financial reports. ShunSin triggered disposition twice in the past two months, so the Q1 loss was already fully disclosed as known information. Even with the known loss, the stock still rose more than 200%. The reason is obvious. For the deeper context, check my earlier post on the subtle implications behind ShunSin’s material announcements clarifying earnings forecasts in the Taiwan market.

2. NVDA 50,000-unit Full-Optical CPO Switch Rerate:

Market rumors first claimed ShunSin landed a major Broadcom order that would drive 2026-2027 EPS up 1,200% (credibility of that news can be judged from the latent analysis above). That speculation alone pushed the stock to around NT$500. On top of that, fresh rumors of accelerated NVDA CPO timelines and Foxconn increasing its full-optical CPO switch orders to 50,000 units. Once you understand ShunSin’s critical role in the Foxconn ecosystem, it becomes clear they can essentially capture almost the entire order.

Here’s a simple forward EPS valuation model for this piece:

50,000 units× USD10k packaging value = USD500 million additional revenue

→ 25% gross margin contributes NT$3.925 billion gross profit

→ After deducting incremental operating expenses (conservative 10%) + 20% tax → contributes approx. NT$1.88 billion after-tax net profit

→ EPS contribution ≈ NT$16.8 (for 2026-2027 combined, based on 112 million shares outstanding)

If we also factor in the existing 800G traditional optical modules plus the Broadcom major order, the overall 2026-2027 EPS outlook points to NT$25–30. Applying a typical 40–60x P/E multiple for Taiwan’s CPO sector, the reasonable target price has enormous upside imagination space.

Summary:

Earnings misses are often the best time to test real conviction in a stock. Once you truly understand ShunSin’s “full-capture” position for high-end orders in the Foxconn ecosystem, you’ll see why NT$500 is just the starting point of the speculation — not the end.

Today’s earnings shakeout is your last easy boarding opportunity before the CPO ramp truly begins! 🚀

#ShunSin# #TWO#.6451 #CPO# #SiliconPhotonics# #NVDA# #Foxconn#

Show more

Nvidia just set up a dedicated zone inside Msscorps ( and locked down 75% of their entire production capacity!

Yesterday at the TSMC Technology Forum, Msscorps was back in the spotlight again. Optical inspection demand is exploding exponentially — their monopoly position is only getting stronger.

BTW, I told you all to buy

yesterday

😉📈🔥 #6830# #Msscorps# #Nvidia# #TSMC#

Show more

Foxconn :

1.800G + Switches 2X this year

2.CPO Switches Mass Production and shipment in Q3.

Supply Chain Mapping: Shunsin (TWE:6451)->Foxconn->NVDA/Broadcom.

IYKYK….

Market rumors: Finisar optical modules price increase by 15-20%, mirroring the recent surge in memory prices. This once again confirms the logic of this chart. 🚀

‘’Finisar’’ is a subsidiary of $COHR (Coherent Corp.). The recent price increase in optical modules signals tight supply in the market, which has significantly enhanced the bargaining power of optical module suppliers

Show more

MSSCORPS ( is dominating the critical optical loss detection niche for silicon photonics (SiPh) and CPO — patents in TW/JP/US, near-monopoly position (>90% share claimed in core light-loss testing for AI/high-speed optics).

SiPh overall TAM is exploding toward ~$8-10B by 2030 (CAGR ~25-29%). The specific test/measurement & optical I/O segment (their sweet spot) is already ~$1.2-1.4B today and projected to hit $2-4B+ in the coming decade with AI data-center/CPO ramp.

With equipment sales (MSS HG units up to ~NT$60M each) + services + licensing, this could drive major forward EPS upside as they scale (rough back-of-envelope: meaningful share capture at scale could push rev hundreds of millions USD with high margins → significant multi-fold EPS growth from current base).

Stock has pulled back ~25-30% from recent highs (~1,000 → ~720). I’m starting to accumulate gradually — grateful the market gave this entry.

(Deeper analysis from sharper accounts like Serenity is far better than mine — no need for me to show off.)

Show more

I know some fellow FinX investors were shocked by Msscorp’s (TWE:6830) 20% pullback (a typical shakeout technique by TW market makers).

Here is some local insight, building on Serenity’s call with additional contributions from @Leoskie_L.

As local TW investors, we are happy to share our insights to help everyone weather this short-term selling pressure. The goal is for everyone to succeed in trading Taiwanese names! 🇹🇼🤝

Show more

Serenity’s High Conviction Bet: ShunSin ( – Pre-Market Supplement:

I have a few quick points to add before the market opens. Hope everyone uses today’s earnings volatility as the perfect chance to get on board!

1. Earnings Loss Interpretation:

According to TWSE (Taiwan Stock Exchange) rules, stocks that enter “disposition” must publish monthly financial reports. ShunSin triggered disposition twice in the past two months, so the Q1 loss was already fully disclosed as known information. Even with the known loss, the stock still rose more than 200%. The reason is obvious. For the deeper context, check my earlier post on the subtle implications behind ShunSin’s material announcements clarifying earnings forecasts in the Taiwan market.

2. NVDA 50,000-unit Full-Optical CPO Switch Rerate:

Market rumors first claimed ShunSin landed a major Broadcom order that would drive 2026-2027 EPS up 1,200% (credibility of that news can be judged from the latent analysis above). That speculation alone pushed the stock to around NT$500. On top of that, fresh rumors of accelerated NVDA CPO timelines and Foxconn increasing its full-optical CPO switch orders to 50,000 units. Once you understand ShunSin’s critical role in the Foxconn ecosystem, it becomes clear they can essentially capture almost the entire order.

Here’s a simple forward EPS valuation model for this piece:

50,000 units× USD10k packaging value = USD500 million additional revenue

→ 25% gross margin contributes NT$3.925 billion gross profit

→ After deducting incremental operating expenses (conservative 10%) + 20% tax → contributes approx. NT$1.88 billion after-tax net profit

→ EPS contribution ≈ NT$16.8 (for 2026-2027 combined, based on 112 million shares outstanding)

If we also factor in the existing 800G traditional optical modules plus the Broadcom major order, the overall 2026-2027 EPS outlook points to NT$25–30. Applying a typical 40–60x P/E multiple for Taiwan’s CPO sector, the reasonable target price has enormous upside imagination space.

Summary:

Earnings misses are often the best time to test real conviction in a stock. Once you truly understand ShunSin’s “full-capture” position for high-end orders in the Foxconn ecosystem, you’ll see why NT$500 is just the starting point of the speculation — not the end.

Today’s earnings shakeout is your last easy boarding opportunity before the CPO ramp truly begins! 🚀

#ShunSin# #TWO#.6451 #CPO# #SiliconPhotonics# #NVDA# #Foxconn#

Show more

I know some fellow FinX investors were shocked by Msscorp’s (TWE:6830) 20% pullback (a typical shakeout technique by TW market makers).

Here is some local insight, building on Serenity’s call with additional contributions from @Leoskie_L.

As local TW investors, we are happy to share our insights to help everyone weather this short-term selling pressure. The goal is for everyone to succeed in trading Taiwanese names! 🇹🇼🤝

Show more