Serenity

@aleabitoreddit

That famous @Reddit WSB Trader now on X.

AI/Semi Supply Chain Analyst

ex. RISC-V FDN, AI research scientist; now trading unknown bottlenecks.

122 Following 296.4K Followers

IMO anything MicroLED is a waste of capital for CPO/photonics exposure over the next year.

Names like ams-OSRAM/AUO/Ennostar/Tyntek/PlayNitride, etc.

Any volume shipments would probably be H2 2028 or H1 2029 if it even takes off from development stage.

You're better looking at them for their other business segments.

Show more

@aleabitoreddit any thoughts on ams OSRAM? They have some interesting application areas in photonics. Is it just hype or they might actually deliver?

Interesting report that I missed that Shunsin (6451) landed $AVGO CPO/SiPH orders…

And their EPS growth rate could reach over 1240%.

Of course this is confidential and is media speculation.

But makes sense that all your top players use Foxconn for optical packaging/test.

Show more

Pretty sure institutions like GS missed Shunsin (6451) at $1.65B for CPO packaging/test/assembly.

Which is why I'm very bullish on it as a completely backdoored, hidden + major beneficiary of $NVDA CPO ramp.

Foxconn is a major supply chain partner among $TSM and $ASX.

But… Shunsin is Foxconn's optical arm, and captures their captive optical and advanced packaging volume.

So they're not explicitly listed anywhere or have direct contracts with Nvidia (but Foxconn does)

But likely soaks up Nvidia CPO + other volumes through Foxconn vertical integration.

Show more

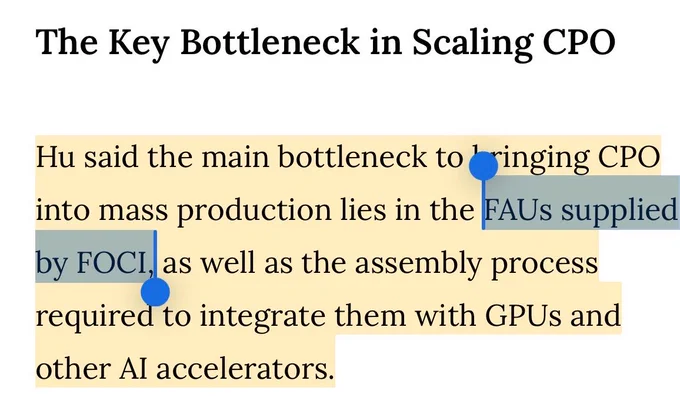

Honestly I’m expecting FOCI (3363) to blow away projections over next two years.

It’s a pretty high conviction position for me medium term at this level.

Since they’re expected to be the leading supplier to $NVDA and $TSM and get frequently cited as a bottleneck for that $91B+ 2028 CPO TAM (GS).

Insane how it’s $3B MC as a critical CPO bottleneck required for scale, while LightWave Logic literally has around the same valuation at $2.7B in development stage.

Show more

@aleabitoreddit This is actually very interesting, their forecast EPS for 2028 is 47 TWD, which give them a PE OF 18, this is insane! Good find!

Now that I think about it more…

Nextronics (8147) is a pretty undiscovered supplier to robotics supply chains like $AMZN too.

So as Amazon scales up, so does their revenue (it’s only ~$200m mc so it should be material if they’re hitting 38-40% gross margins).

I was only focusing on $NVDA CPO supply chains as their largest growth vector earlier.

But I do think Amazon’s robotics program have the simplest route for mass production since each one they make internally lowers opex, cuts headcount, and improves profitability.

And their whole ecosystem should benefit.

Show more

@Dog_Ziller I actually think $AMZN for robotics is extremely underrated.

Since since there’s immediate practical upside to lower opex + headcount for automation.

But for general purpose $TSLA, Unitree, Figure, Boston Dynamics, Agibot, Agility, and others should do well.

Show more

Imo harmonic drive (6324) one of the better humanoid exposure names at $4B valuation listed in GS research report.

Personally I picked some up for exposure.

Chinese competitors might be used for mass production.

But personal preference in investing in Western supply chains + build them up.

Show more

@Dog_Ziller I actually think $AMZN for robotics is extremely underrated.

Since since there’s immediate practical upside to lower opex + headcount for automation.

But for general purpose $TSLA, Unitree, Figure, Boston Dynamics, Agibot, Agility, and others should do well.

Show more

“Robotics may be the biggest product category of all time” - $CDNS CEO.

“The projection is $25 trillion. The whole GDP of the world is $110 trillion. So this is huge if this happens.”

Extremely bullish on robotics/humanoids directionally.

But maybe it’s time for $TSLA and America to really start prioritizing how we build it outside Chinese supply chains?

Show more

What an insane day for photonics.

$SIVE up 31.3%

$TSEM up 23.1%

$AAOI 20.01%.

It feels like a lot… but this just means you’re early to the next supercycle and there’s a lot of room to go.

Lot of people on X ask what’s next after $SNDK?

Here they are.

Show more

Woah, this list compiled by you all….

Actually cooked so hard.

Many are up 2-6 times already.

Serenity's Followers Favorite Stock Parabolic Growth ETF:

The most anticipated ETF of all time:

$TRT - $5.88

$HGRAF - $4.49

$SIVE - 9.9 SEK

$QURE - $17.21

$AEHR - $45.08

$ENVX - $5.07

$ASPI - $4.2

$EONR - $11.79

$LPK.DE - 6.59 EUR

$MITK - $13.9

$EQR.AX - .315 AUD

$WATT - $15.8

$VLN - $1.16

$BZAI - $1.79

$TMC - $4.59

$ALCJ - $74.57

$POET - $6.11

$AAOI - $108.86

$ADUR - $10.37

$P4O.DE - 6.85 EUR

$PLAB - $40.87

$FLY - $33.16

$LASR - $60.7

$AL2SI - 28.70 EUR

$ENAFF - $1.71

$VPG - $44.7

$EOS.AX - $9.00

I haven't heard of 1/3rd of these names, but if my followers have high conviction that their name will 10x...

So do I.

Show more

I like how $HPS.A is just a vertical line up 2-3% increase every day since my thesis post.

Just 20 CAD away before it hits triple digit returns.

The current bottleneck: Transformers/Switchgear.

Trade Idea: Long Hammond (~2.2B CAD / ~$1.5B USD) at 184 CAD.

They dominate the market for:

-Transformers (dry, multi year bottleneck ~23% of market),

-serve to switchgear (2-3Y bottleneck)

-and manufacture liquid too (5Y, larger bottleneck)

I personally anticipate components price hikes like NAND, as $AMZN, $MSFT and others compete for allocation.

You might have seen: “Half of US data center builds have been delayed or canceled, growth limited by shortages of power infrastructure”…

Then you go further:

“To address shortages… Canada, Mexico… became the biggest suppliers of high-power transformers for AI data centers to AI data centers”

Guess who is in Canada (Guelph).. Mexico (Monterrey 3 and 4)… and the US?

Hammond

Then here’s the reason the articles cite why hyperscaler DB buildouts are falling apart:

“Major reason behind these setbacks is the availability of key electrical components — such as transformers, switchgear”.

Institutions are probably looking at Powell, Eaton, and others… but little do they know?

Companies like these actually buy Hammond’s transformers to put inside their own switchgear (“strong sales into data centres, switchgear manufacturers")

Their market share over the transformers market is actually pretty large (eg. ~23% dry).

The most compelling signal:

-> 122% Y/Y 2025 backlog increase. And we can infer this to be 1B+ CAD.

Eg. company achieved 898m CAD in sales in 2025, capacity ceiling. Management said close of Q3 2025 orders were valued at 53% of the entire closing third-quarter backlog.

Given that Q4 2025 revenue was 254 million and the backlog is "more than doubled," we can infer a total backlog value exceeding 1 billion CAD.

Also:

“Gross margin compression last year was due to the buildout of their Mexico facility, but both gross margins are expected to increase and the facility expansions are expectied to turn into accelerated revenue Q2 2026)” which is now.

Downside is if raw material costs (copper, electrical steel) spike again, but given this bottleneck, they can price hike.

Personal FWD P/E estimates would be ~18-21 for 2026, <15 for 2027 from volume ramp.

But I think it’s possible to hit single digit fwd P/E if they do price hikes mixed with hyperscaler emergency orders. But that might get a little mixed with the new acquisition.

Regardless still looks cheap.

Just a TLDR:

$AMZN, $MSFT, $META, $GOOGL, $ORCL datacenter are being bottlenecked because of a lack of transformers/switchgear.

Seems like markets missed this little player with large market share, despite backlog visibility and increasing revenue from capacity expansion coming online.

I personally found it pretty compelling, so I went long.

Just sharing my personal thoughts, of course DYOR before making any decisions yourself.

Show more

$AAOI is now up ~6-7x at $200+.

Feels like nobody else was long last year aside from me and like two other people on X?

Remains one of my top high conviction optical longs moving forward into 2027 due to massive revenue ramp + Made in America supply chains.

Show more

Just in case you were wondering $TSEM reported extra prepayment ($290M) to secure capacity.

Downstream foundry capacity squeeze directly translates to an immense demand for raw substrates upstream with $SOI (more revenue).

My optical picks are very interconnected.

Show more

@aleabitoreddit Is $SOI already facing substrate supply tightness?

If CPO scale-up accelerates, will Tower sign a longer-term strategic supply agreement with them, or stick to the spot market for flexibility?

Show more

And exactly 2 months later.

$TSEM is trading at $250+ post earnings.

The vast majority of my picks keep making ATHs every day after there’s more time for the thesis to play out.

Did you listen anon?

Show more

I'm long $TSEM, the $TSM of photonics.

My top two picks for CPO are $SOI and Tower Semi.

Given the $NVDA GTC catalyst on new photonic related architecture next week:

I expect Tower Semi to get a huge catalyst.

Nvidia laready directly collaborated with Tower to scale 1.6T silicon photonics last month (hint hint for GTC), likely pushing the downstream players to use it.

And now, Tower is the leading supplier of 1.6T SiPh PICs and the primary foundry for scale-up CPO architectures. (the other being global foundries)

From my forward est:

2028 Forward P/E: ~16.8x to ~18.1x

(Tower set a target $2.84B revenue by 2028, with ~31.7% operating margin, ~$750M in net profit)

The thing to note is over 70% of their planned SiPh capacity is already reserved through 2028. And photonics haven't even ramped up yet.

So, I expect them to strongly beat earning projections due to extreme photonics scaling + allocations price hikes that's not modeled into projections.

Also, $TSEM is heavily de-risked by 70% of capacity already being reserved. MC is likely due to $TSEM being a very obscure upstream player in the photonics supply chain.

But I expect the $NVDA GTC conference to be that catalyst that brings it to premium valuations.

I'm long $TSEM as an asymmetrical upside for upstream photonics foundry layer.

Show more

$NBIS earnings were stellar and it’s now trading $200+ premarket.

Reiterated $7-9B ARR in 2026. 40% adj. EBITDA margin projections, which is vastly outperforming expectations.

4 GW contracted capacity. $6.3B capital secured by $NVDA off solid financial offering structures.

Glad my high conviction Neocloud pick is performing wonders and happy management is executing so well.

In the words of Jensen: “Nebius will take care of you”

Show more

Wow, $SIVE to be listed in the MSCI Global Small Cap Index.

This is overwhelmly positively as it triggers more passive inflows as the MC grows.

Rebalancing takes places May 29th.

@aleabitoreddit Now it’s also being listed to the MSCI Small Cap Index.

Swedish article:

To make things even spicier.

$SIVE is run by UC Berkeley CEOs and $LITE executives.

And the ownership cab table is now controlled by American institutions/investors.

I’d expect things to speed up on NASDAQ listing as American institutions are heavy fond of executive teams + cap tables like this.

US/Silicon Valley is now speedrunning a Swedish in name photonics company.

Show more

Did you know this about $SIVE?

Neeraj Chopra, VP of Global Operations at Sivers Semiconductors, spent 19 years as Vice President at Lumentum ($LITE) from 1999–2018.

$LITE is one of the greatest success stories in photonics.

That same expertise is now inside $SIVE’s team.

Show more

To answer that question.

I’ll just float some historical data out there with laser chokepoints:

$LITE went from $3B -> $15B -> $80B in 2 years from 2024.

$AAOI went from $770M -> $15B in 1 year from 2025.

$SIVE is $1.6B today in 2026.

There’s not many in the world and lasers are the absolute center of photonics.

Each owned a specific chokepoint from optical architectural shifts.

$LITE for EML.

$AAOI for cw 800g/1.6T pluggable

and now $SIVE for cw CPO.

Show more

@aleabitoreddit So is $SIVE the best play for CPO

People wonder why I'm focusing on non-US markets recently.

Why? CPO is my #1# thematic long.

Markets don't know yet, the sudden paradigm shift in photonics...

I was one of the only to frontrun the current supercycle in 2025 w/ $AAOI @ ~$30, $LITE ~$300s, and $AXTI at ~$13 on X....

With the actual receipts and thesis that others can't show.

CPO goes from ~$0. To $91 Billion TAM opportunity.

In the next 1 1/2 years from GS research.

While overall optical market reaches $154B.

Many players that had little exposure to the current photonics cycle at all:

-> In Europe with high-end lasers design like $SIVE or $SOI with substrates.

-> In Taiwan with Foci (3363), Nextronics (8147), Shunsin (6451) and others for optical components and foundries.

-> In Japan with laser mass production, substrates, and chemicals.

Are suddenly the new dominant players for CPO.

As for US players, there's not much exposure. But the existing ones like $LITE, $COHR still get upside from CPO as that's their new growth vector.

My contrarian thought process on current players:

Is that most of their valuation is priced in huge legacy pluggable revenue that will inevitably face cannibalization over time, so re-rating potential is less unless someone uses leverage.

A lot of these new purer play CPO names go from 0 to 100 extremely quickly one mass production starts H2 2026 for scale out (as a revenue bridge) into H2 2027 for scale up (massive growth driver).

Markets usually price things in 8-12 months ahead of time too...

I have high conviction thematically in my supply chain research despite any market volatility leading up until then.

Show more

So here's the napkin math I did on Nextronics (8147) when I went long.

They're the $NVDA CPO supplier for CPO connectors and cage thermal modules.

And I modeled around 2 FWD p/e for 2028, which is why I think risk-reward is very compelling for a potential 10x rerating to ~$2B+ MC in 2028.

Just for their CPO exposure:

-> CPO connector runs roughly $15 to $25

-> ELS thermal cages, maybe ~$50 from est.

18 units per switch: 18x50 = ~$900

CPO Connectors: 72 Optical Engines per switch 72 x $15 = $1,080

(If $NVDA scales their Spectrum-X switch, it goes to $1,920 for CPO connectors).

Total Nextronics Content: ~$1,980 (rounded to $2k for calculations) in conservative case.

Implied BOM % of rack: 0.08%. Maybe ~1.5% of switch.

This looks microscopic to institutions so it probably is ignored.

Is it material to Nextronics, a ~$200m company?

Yes, absolute massive.

For calculations: Applying 50% haircut to Nextronics' share of the Nvidia connector market/cage market because of multi-source.

And I’m using GS projections, and assuming $AVGO, $MRVL, ASIC CPO ecosystem is 30% size of $NVDA.

Net Income Margin: 22.4% (at 38% GM)- 24.0% (at 40% GM).

But going off other projections from just, a rack shipments:

2026: CPO revenue ~10.1M, net income (22.4%)

~2.26M + $12.5M base = $14.7M (540k units for connectors, cage, 40K units, already divided by 50%)

2027: CPO revenue: ~$172M, net income (22.4%): ~$38.53M = $51.03M (~8M units for connectors, ~1.03M units for cage)

2028 scale up expansion: CPO revenue: $450m, net income: $100.93M, ~$11.3M base (~40M units for connectors, 2.98M unit for cages, eg. Nvidia ELS volume is 19.9M)

So implied fwd p/e 15.4x for 2026, 4.45x for 2027, 2x for 2028.

Of course at scale, blended margins might go down, there might be other players bringing market share down to like 25%, etc. and projections might be more or less than GS.

But regardless seems highly asymmetrical even if I'm off by a whole 50%.

2028 is usually the massive re-rating for CPO players, 2026 is still really early.

Hope my math is right, but 20x fwd p/e multiple would be $2.26B MC.

Even if we drop:

-> market share to just 15%.

-> compress their net income margin down to 14%.

-> connector ASP to $10.

At a 20x multiple, the stock would still achieve a ~4.5x return to a $1B+ market cap.

We'll see if this is right or not. (NFA, just speculative financial modeling)

Show more

@aleabitoreddit It'd be great if you included your revenue models and projections whenever you share positions you enter.

I know in the past you've said it's to simplify for retail, but easier to build conviction when we can see your reasoning and actual numbers (and allow us to double check).

Show more

Random CPO related names I like:

- $SIVE

- Foci (3363)

- $TSEM

- Browave (3163)

- PCL (4977)

- $AXTI

- Msscorps (6830)

- $IQE

- Shunsin (6451)

- Furukawa Electric (5801)

- $MTSI

- Nextronics (8417)

- $LITE

- $COHR

- FitTech (6706)

- $GFS

- $ASX

- LandMark (3081)

- $SOI

Disclosure: I own most, not all though.

Show more